Richardson Group

Wealth Protection

Live the retirement that you've earned.

Featured on:

We're Here To Help

Get to know Philip and Richardson Group Wealth

Protection

Join Phil, George, Jordyn, Halle, and the entire team at Richardson Group Wealth Protection for a behind-the-scenes look at their work in Lancaster, Pennsylvania. Discover how hard work, adaptability, and strong family values have built this award-winning financial firm and continue to inspire everything they do to help clients achieve lasting financial peace of mind.

Watch our story and see how family, purpose, and passion drive everything we do at our financial and retirement planning company.

At Richardson Group Wealth Protection, we believe financial planning is about more than numbers — it’s about people, families, and futures.

Every conversation starts with listening, understanding your goals, and building a plan that fits your life. From our roots here in Lancaster, Pennsylvania, to the clients we serve across the country, we’re proud to bring clarity, compassion, and confidence to every stage of retirement planning.

About Us

Making Financial Planning Simple, Personal, and Purposeful

Founded in 1996 by Philip L. Richardson, an M.S. in Financial Planning, Richardson Group Wealth Protection was built on a simple idea: financial planning should be approachable, personal, and focused on what truly matters—helping seniors to simplify their retirement planning through safe, guaranteed strategies.

As a family-owned firm in Lancaster County, PA, our office feels more like a home than a corporate space. Philip’s two daughters, Jordyn and Halle, are proud members of the team, helping us create a warm, inviting environment where every client feels welcome and cared for.

We specialize in helping individuals and families find clarity and confidence in their financial future, using safe, guaranteed annuity products and proven retirement strategies. As fiduciaries, we’re legally and ethically committed to always putting your best interests first.

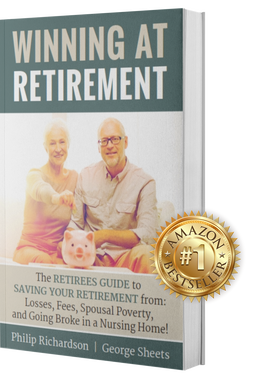

Get Your Complimentary Copy of Phil's Bestselling Book

Error: Contact form not found.

Phil’s Amazon best-selling book, Winning At Retirement, will change the course of your life. Get the tools you need to live an amazing retirement today by requesting a free copy.

Our Approach Is Different

Our team has worked with countless retirees just like you. Our goal is simple: make sure you get the retirement that you’ve earned. We serve Lancaster, York, and Dauphin counties.

No Investment Fees

Would you buy a house if you had to pay a lifetime annual fee to the broker who sold you your home? Of course not. We'll show you how to maximize your returns without fees. We encourage you to visit us for a free consultation to explore investment options that do not charge you a fee.

No Market Losses

We decided 30 years ago to only use products that don't subject your money to market losses, the same way that CDs do not expose you to market losses. Your funds get part of the gains of the underlying index, for example the S&P 500, but your investment does not lose any value during market losses.

Your Lifetime Income

After you retire, you should consider if other income streams, aside from your pension or social security, are necessary. We've built guaranteed income plans for hundreds of retirees just like you. We offer guidance on incorporating annuities into your retirement plan to provide a stable, guaranteed income flow.

Reduce Your Taxes

Our Senior Tax Strategies division offers free-tax consultations to identify ways to reduce your tax burden and optimize your portfolio for current and future tax situations. We serve your needs with accurate and efficient income tax preparation of federal, state, and local income tax returns.

Get the retirement that you deserve.

The first step is picking up the phone.

Do You Pay Advising Fees?

Philip Richardson

Your Retirement Specialist

As President of the company, Philip Richardson has been a prominent figure in the financial services industry since 1996, the year he established his current financial advising company, Richardson Group Wealth Protection. His commitment to serving the needs of seniors also led him to found Senior Tax Strategies, LLC in 1999. He has a strong educational background, holding a Master of Science (M.S.) in Financial Planning.

As a dedicated educator, Philip has shared his expertise with thousands of retirees through various channels, including seminars, workshops, and a weekly radio show. His goal has always been to help seniors safeguard their savings, minimize taxes, and make well-informed financial decisions with confidence. He is also a respected author, co-authoring the book Winning at Retirement.

Philip resides in Lancaster, Pennsylvania, where he demonstrates a strong commitment to family, fitness, and community engagement. He upholds a disciplined, health-focused lifestyle and frequently trains in his home gym alongside his longtime business associate, George Sheets. Their shared dedication to personal excellence and professional integrity reflects the values that guide Philip’s work and leadership.

Jordyn Richardson

Jordyn Richardson serves as Executive Vice President at Richardson Group Wealth Protection, where she has been helping clients achieve financial confidence. She works directly with clients on all aspects of their financial planning, with a special focus on retirement income strategies, Social Security optimization, and long-term wealth preservation. Jordyn is especially passionate about empowering women—particularly single and retired women—to take control of their financial futures and feel secure in their retirement years.

As the author of You Are Not Alone, a book written specifically for single retired women, Jordyn combines her professional expertise with her passion for helping others feel supported and capable in their financial decisions. She partners closely with clients to create personalized retirement and protection strategies designed to help them meet their goals and enjoy the lifestyle they’ve worked hard for.

A proud Penn State graduate, Jordyn brings the same dedication she shows her clients to her community. She volunteers weekly as a small group leader in LCBC Church’s high school ministry. Outside of work, Jordyn enjoys traveling, hiking, and skiing with her husband, Ross—and their dog, Reilly, who often joins her at the office.

Halle Richardson

Halle Richardson plays an important role here at Richardson Group Wealth Protection in helping clients with estate and retirement planning. As Executive Vice President at the company, she specializes in guiding clients through strategies to protect and grow their wealth, while ensuring their plans remain aligned with their long-term goals. Halle is especially passionate about helping individuals feel confident and secure in their legacy planning, providing peace of mind for both themselves and their loved ones.

Halle supports clients by managing communications and coordinating annual reviews to help keep their financial strategies on track. She is committed to delivering exceptional service and continues to expand her knowledge to better assist clients with comprehensive financial planning.

When not at work, Halle enjoys connecting with her community as a board member of The Stone Independent School and as a volunteer in the historic gardens at Rock Ford. She also loves attending Renaissance Faires and spending time gardening—a hobby that reflects her passion for cultivating growth in all areas of life.

George Sheets

As Executive Vice President at Richardson Group Wealth Protection, George Sheets has been serving clients in the financial planning industry since 2003, bringing a wealth of experience and a passion for helping middle-class families make sound financial decisions about college planning, retirement, and long-term security. Before entering the financial field, George spent 25 years in executive management roles across various industries in Central Pennsylvania.

A graduate of Millersville University with degrees in Computer Science and Economics, George went on to earn his Master of Business Administration from Lebanon Valley College in 1990. Throughout his 20-year financial planning career, he has been recognized with numerous national awards for his commitment to excellence and client service. He co-authored the book Winning at Retirement with Philip Richardson.

George and his wife, Jennifer, are lifelong Lancaster County residents and live in East Hempfield Township with their Yorkshire terrier, Tigger. They attend Victory Church in Lancaster and enjoy spending their free time outdoors—walking, running, bicycling, and socializing with friends. George is also active in his community through volunteer work with the Lions Club and as a member of the Elks and Moose Clubs.

John Wood

Since joining Richardson Group Wealth Protection, John Wood has played an active role in connecting with the community through educational seminars and one-on-one consultations, focusing on topics such as Social Security, Medicare, taxes and retirement. Holding an insurance license, he enjoys helping individuals and families understand their financial options and make confident decisions for the future.

In his free time, John enjoys spending time with his wife, Deb, and their daughter, Lauren. Together, they love traveling—especially to their condo in Ocean City, Maryland. When he’s not with family or on the road, you can often find John out on the golf course or playing with the family’s dogs, George and Elaine, named after the Seinfeld characters.

Jennifer Sheets

Jennifer Sheets has been an integral part of Richardson Group Wealth Protection for a decade, celebrating her 10th anniversary with the firm. Working alongside her husband and colleague, George Sheets, she manages his workshop/seminar events.

Her responsibilities involve managing workshop appointment scheduling and registration processes, as well as handling appointment reminder calls to ensure optimal communication and client service.

Outside of the office, Jennifer leads an active and community-focused lifestyle. She maintains a rigorous fitness routine, which includes walking over 4 miles daily and working out at the gym. Committed to her community, she volunteers her time at Fresh Express in Columbia, PA, a program that delivers nutritious food to communities in our region. Jennifer is also an active member of Victory Church in Lancaster, where she participates regularly in the women’s bible study program.

Jim Slupe

James Slupe is an IRS-registered tax preparer and wealth protection professional with extensive experience serving individuals and small businesses in the Lancaster and York County, Pennsylvania areas. Holding a bachelor’s degree, a life insurance license, and a Chartered Life Underwriter (CLU) designation, he specializes in tax preparation, planning, bookkeeping, estate and trust taxes, and annuities.

He has a long career working in the insurance industry, initially focusing on life insurance for young families before transitioning to annuities, primarily serving seniors.

Jim has worked alongside Philip Richardson since 1996 and has served as the president of a professional insurance organization known for its training programs.

In the community, he is actively involved as the treasurer of a private club in Lancaster. Outside of his professional life, James is a family man, enjoying time with his wife, Penny, and their five children. A former golf enthusiast, he is also a big Penn State fan, previously attending games in his RV. In addition, he is a skilled bridge player.

Protect your legacy with confidence.

Schedule a meeting today!

Contact Us

- Address: 450 Murry Hill Drive Lancaster, PA

- Phone: (717) 394-0840

- Email: Client@RichardsonGWP.com

Client@RichardsonGWP.com

450 Murry Hill Drive

Lancaster, PA 17601

Hours: Monday – Thursday | 9:00 am – 4:00 pm

Friday | 9:00 am – 2:00 pm